If investing were a dinner party, individual bonds would be the carefully plated entrée, while a bond fund would be the buffet. Both can feed your portfolio. Both can help with income, diversification, and risk management. But they do the job in very different ways. And if you pick the wrong one for the wrong reason, your “safe” fixed-income strategy can turn into an expensive lesson with a side of confusion.

That is why the debate over owning individual bonds vs. owning a bond fund matters so much. On paper, both live in the same neighborhood: fixed income. In real life, they behave differently when it comes to maturity, liquidity, diversification, fees, control, and how much hand-holding you want from your investments. One gives you a known finish line. The other gives you scale, convenience, and built-in variety. Neither is automatically better. The better choice depends on what job you need the investment to do.

If your goal is to match future cash needs with precision, individual bonds can look awfully attractive. If your goal is broad exposure, easy management, and a lower barrier to entry, a bond fund may be the smarter and saner pick. Let’s break it all down without making your eyes glaze over like a stale donut in a conference room.

What Is the Difference Between an Individual Bond and a Bond Fund?

An individual bond is a single debt security issued by a government, municipality, or corporation. You lend money to the issuer, the issuer pays you interest, and if all goes according to plan, you receive your principal back at maturity. You know the issuer, the coupon, the maturity date, and the face value. It is a one-security relationship, for better or worse.

A bond fund, by contrast, pools money from many investors and uses it to buy a collection of bonds. That fund may be a mutual fund or an exchange-traded fund (ETF). Instead of owning one bond directly, you own shares of a portfolio that may hold dozens, hundreds, or even thousands of bonds. The fund may focus on U.S. Treasuries, corporate bonds, municipal bonds, mortgage-backed securities, short-term bonds, or a broad blend of fixed-income assets.

That basic structural difference explains almost everything else. Individual bonds offer control and a defined maturity date. Bond funds offer diversification, professional management, and easier access. So the real question is not “Which one is best?” It is “Which one fits your goal, your budget, and your tolerance for doing homework?”

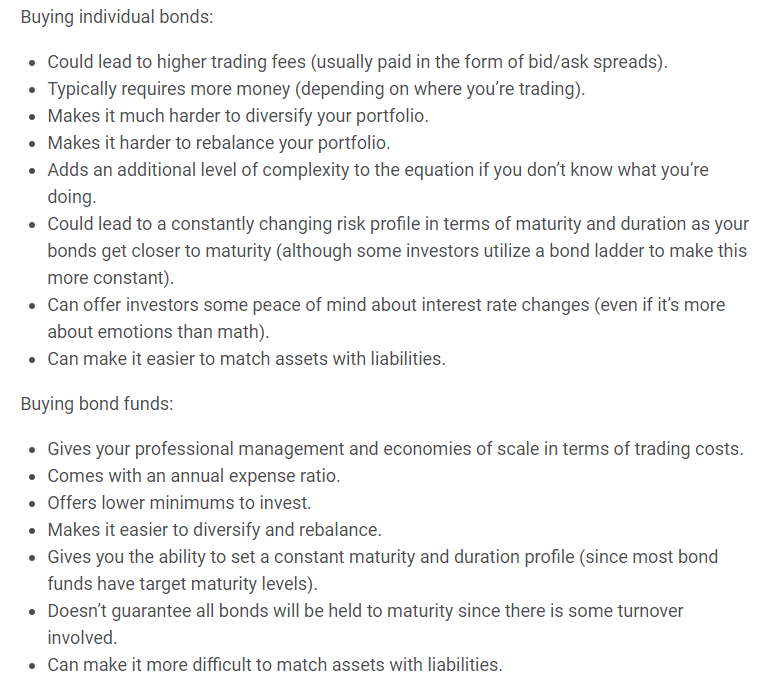

Why Some Investors Prefer Individual Bonds

1. You Get a Predictable Maturity Date

This is the biggest selling point. If you buy an individual bond and hold it to maturity, you generally know when your principal is scheduled to come back, assuming the issuer does not default and the bond is not called early. That makes individual bonds useful for planning around future liabilities.

Say you know you will need $25,000 in four years for your child’s tuition, a home project, or a tax bill that is about as welcome as a skunk at a garden party. Buying bonds that mature around that time can make sense because they can be matched to the date of the need. That type of planning is much harder with a traditional bond fund, which does not mature as a whole portfolio on a single date.

2. You Have More Control

With individual bonds, you choose the issuer, the credit quality, the maturity, the tax treatment, and the structure. You can build a ladder of bonds with staggered maturities. You can focus on Treasuries, investment-grade corporates, or municipal bonds. You can decide whether you want shorter-term stability or longer-term yield potential. In other words, you are the portfolio manager, which is exciting if you enjoy control and less exciting if you already have enough spreadsheets in your life.

3. No Ongoing Fund Expense Ratio

Individual bonds do not come with an annual expense ratio the way bond mutual funds and bond ETFs do. Once you buy the bond, you are not paying a manager every year to oversee it. That can be appealing for cost-conscious investors.

But here is the catch: “no expense ratio” does not mean “no cost.” Individual bond investors can still face markups, markdowns, commissions, and bid-ask spreads, especially in less liquid parts of the market. So yes, you may avoid recurring fund expenses, but you do not magically escape the laws of finance.

Where Individual Bonds Can Be Tricky

1. Diversification Is Harder Than It Sounds

Owning one bond is simple. Owning enough bonds to build a properly diversified portfolio is a very different story. A single corporate bond leaves you exposed to one issuer. A handful of bonds may still leave you concentrated by sector, credit profile, or maturity range.

Many bonds trade in $1,000 face-value increments, but assembling a diversified portfolio can require much more capital than that. If you want exposure across many issuers and maturities, the dollar requirement rises fast. That is one reason bond funds are so popular: they let smaller investors buy broad diversification in one trade instead of trying to build a mini fixed-income empire one CUSIP at a time.

2. You Need to Do More Research

When you own individual bonds, you are responsible for knowing what you own. That means reviewing credit quality, call features, maturity dates, tax treatment, and how the bond fits into your broader asset allocation. If the issuer’s financial condition changes, you need to notice. If interest rates move, you need to understand what that means for your portfolio. If a bond can be called away, you need to factor that into your expected income.

For some investors, that level of involvement is a feature. For others, it is a full-time hobby they never asked for.

3. Selling Before Maturity Can Be Painful

A common myth is that individual bonds are immune to market volatility. Not true. Their market prices still move when interest rates change, credit conditions shift, or liquidity dries up. The reason individual bond investors often feel calmer is that if they hold to maturity, they may receive par value back even if prices moved around along the way.

But life does not always cooperate with hold-to-maturity plans. If you need cash early, you may have to sell at a loss. And depending on the market, selling an individual bond can be less convenient than hitting the sell button on a bond ETF.

4. Income Timing Is Less Flexible

Most individual bonds pay interest semiannually. That is fine for many investors, but not always ideal if you want smoother monthly cash flow. Bond funds often distribute income monthly, which some retirees and income-focused investors find easier to work with.

Why Bond Funds Appeal to So Many Investors

1. Instant Diversification

The clearest advantage of a bond fund is diversification. One fund can hold a huge number of bonds across issuers, sectors, maturities, and credit levels. That lowers the impact of any single bond default or downgrade. For investors with limited capital, this can be a major win.

Instead of buying 20 or 30 bonds individually, you can buy one fund and gain broad exposure. That convenience is hard to beat, especially for people who want fixed income to do its job quietly in the background rather than become a second career.

2. Easier Access and Lower Minimums

Bond funds usually require less money to get started than a diversified portfolio of individual bonds. You can often buy a bond ETF for the price of a single share, or enter a bond mutual fund with a modest minimum. That makes bond funds more accessible for younger investors, smaller accounts, and anyone who would rather not tie up a large chunk of money in a handful of securities.

3. Professional Management

Fund managers handle credit analysis, portfolio construction, trading, and reinvestment decisions. In active funds, they can shift exposure as opportunities change. In index funds, they track a market segment efficiently and usually at a low cost. Either way, the day-to-day management burden falls on the fund rather than on you.

4. Better Convenience and Liquidity

Bond mutual funds generally offer daily liquidity, while bond ETFs trade throughout the day on exchanges. That is often more convenient than selling an individual bond in the secondary market. Bond funds also make reinvestment easier. Income distributions can be reinvested automatically, which helps investors compound returns without extra manual work.

The Drawbacks of Bond Funds

1. No Guaranteed Principal Back on a Specific Date

This is the issue that makes many investors fall back in love with individual bonds. A traditional bond fund does not mature on one fixed date, so there is no promise that you will get a specific principal amount back at a specific time. The share price, or net asset value, rises and falls with the market.

That means bond funds are often less precise for matching a known future expense. If rates rise and your fund’s net asset value drops, you cannot simply point to a maturity date and say, “No worries, it all snaps back then.” That is not how regular bond funds work.

2. Ongoing Fees

Bond funds charge expense ratios, and some may involve additional trading or sales costs depending on the structure and where you buy them. Low-cost index funds can be quite efficient, but fees still matter because every basis point comes out of returns. Over time, those costs can nibble away at income like a very polite but persistent squirrel.

3. Less Customization

When you buy a bond fund, you are buying the manager’s or index’s portfolio rules, not your own exact preferences. You may not control every issuer, every maturity date, every tax detail, or every reinvestment choice at the security level. That is the tradeoff for convenience.

4. Yield Can Be More Complicated

With an individual bond, yield to maturity is tied to that specific security and its path to maturity. In a bond fund, the reported yield is a portfolio-level snapshot, and the underlying bonds may be bought, sold, replaced, or rolled over. So while fund yield metrics are useful, they are not the same as the locked-in math of holding one bond to maturity.

Individual Bonds vs. Bond Funds: Quick Comparison

| Category | Individual Bonds | Bond Funds |

|---|---|---|

| Maturity date | Yes, each bond has one | No fixed maturity for traditional funds |

| Principal certainty | More predictable at maturity if no default | Share price fluctuates |

| Diversification | Harder and more expensive to build | Easy and built in |

| Minimum investment | Often higher for true diversification | Usually lower |

| Management | Self-directed | Professional or index-based |

| Liquidity | Can be limited in some markets | Generally easier to trade or redeem |

| Income frequency | Usually semiannual | Often monthly distributions |

| Fees | No ongoing fund fee, but trading costs may apply | Expense ratios and possible trading costs |

| Customization | High | Lower |

When Individual Bonds May Be the Better Choice

Owning individual bonds may make more sense if you have a specific date-based goal, a larger amount to invest, and the interest and ability to manage the portfolio. They can be especially useful for liability matching, laddering strategies, or tax-aware municipal bond planning.

For example, a retiree who wants known principal repayments over the next seven years may prefer a ladder of Treasuries or high-quality bonds. A high-income investor in a high-tax state may want hand-picked municipal bonds. An experienced investor who enjoys monitoring credit quality may also prefer owning the securities directly.

When a Bond Fund May Be the Smarter Choice

A bond fund can be the better option if you want broad diversification, low maintenance, and easy access with less money. That often describes younger investors, retirement savers making regular contributions, and people who want fixed income exposure without building a ladder themselves.

Bond funds also make sense for investors who want their bond allocation to act as a stabilizer in a diversified portfolio, not as a hand-built engineering project. If your main goal is to own quality fixed income and rebalance occasionally, a low-cost bond fund or bond ETF can be extremely practical.

The Hybrid Option: Why Many Investors Use Both

Here is the plot twist: you do not always have to choose one side and start a family argument at Thanksgiving. Many investors use both.

A common hybrid approach is to keep a core allocation in a broad bond fund for diversification and liquidity, while using individual bonds for near-term liabilities or a custom ladder. For instance, you might hold a U.S. aggregate bond ETF for core exposure and a ladder of Treasuries maturing over the next three to five years for planned withdrawals. That gives you convenience where it matters and precision where it counts.

There are even target-maturity bond ETFs that try to blend some of the features of individual bonds and funds. These products can offer diversification while also having a defined maturity year. They are not identical to owning a single bond, but they can be useful for investors who want something between full do-it-yourself bond ownership and an open-ended bond fund.

Mistakes Investors Make With Both

- Assuming bonds cannot lose money: They can, especially if sold before maturity or if credit problems arise.

- Chasing the highest yield: Higher yield often means higher credit risk, higher duration risk, or both.

- Ignoring fees and spreads: Bond funds have expense ratios, and individual bonds can come with hidden trading costs.

- Confusing stability with certainty: A bond fund can still be volatile. An individual bond can still default.

- Forgetting taxes: Taxable bonds, municipal bonds, and bond fund distributions can all be taxed differently.

Bottom Line: Which One Wins?

Owning individual bonds vs. owning a bond fund is not a battle with one universal winner. Individual bonds shine when you want control, a predictable maturity date, and a portfolio built around known cash needs. Bond funds shine when you want instant diversification, easier investing, lower starting costs, and professional management.

If you need precision, individual bonds may be your best friend. If you need simplicity and scale, bond funds may deserve the crown. And if you are like many investors, the smartest answer may be a little of both. In fixed income, the winning strategy is usually not the one that sounds the fanciest. It is the one that best matches your goals, your time horizon, and your tolerance for doing the heavy lifting yourself.

Investor Experiences and Practical Lessons From the Real World

One of the most common experiences investors have with individual bonds is the quiet comfort of knowing when their money is supposed to come back. Picture a couple a few years from retirement. They do not want to guess what the stock market will do next spring, and they definitely do not want to sell stocks during a bad year just to cover living expenses. So they buy a ladder of high-quality bonds maturing every year for the first five years of retirement. Their reaction is usually less “Wow, thrilling!” and more “Finally, I can sleep.” That is the beauty of predictability. Individual bonds are not flashy, but they can be wonderfully boring in all the right ways.

Now compare that with a younger investor in their 30s building wealth through monthly contributions. This person may not have enough money to buy a diversified basket of individual corporate bonds without concentrating too much in a few issuers. A broad bond ETF becomes the practical choice. They can invest steadily, reinvest distributions automatically, and avoid the hassle of researching each bond one at a time. Their experience is often shaped by convenience. They are not trying to perfectly match a future bill due on June 15, 2031. They are trying to build a long-term portfolio without creating extra homework every weekend.

Then there is the investor who learns the hard way that “safe” does not mean “simple.” This often happens when someone buys a bond fund expecting the share price to behave like a savings account. Interest rates rise, the fund’s value drops, and panic sets in. The investor says, “Wait, I thought bonds were the calm part of my portfolio.” The lesson here is important: bond funds are collections of bonds, but fund shares still fluctuate. They can be excellent tools, but they are not frozen in place. Investors who understand duration and interest rate sensitivity ahead of time usually handle this experience much better.

On the flip side, some people discover that owning individual bonds is more work than they bargained for. They liked the idea of avoiding fund fees, but they did not enjoy comparing yields, reading about credit quality, checking call features, and dealing with thin trading in certain corners of the bond market. Their portfolio started to feel less like “fixed income” and more like “part-time analyst job.” For these investors, bond funds often become the cleaner solution, even if that means paying a modest expense ratio.

A final real-world lesson is that many experienced investors eventually stop treating this as an either-or decision. They use individual bonds for short- and medium-term cash flow needs, then use bond funds for the rest of their fixed-income allocation. That blended approach often feels less ideological and more practical. And practical usually wins. The truth is, the best bond strategy is the one you understand well enough to stick with when markets get noisy, headlines get dramatic, and somebody on the internet starts yelling that one approach is “always better.” It almost never is.