Quick answer: Most personal and business checks are considered “stale” after 6 months (180 days), U.S. Treasury checks are good for 1 year, USPS money orders never expire, and traveler’s checks don’t expire. Cashier’s and certified checks are a special casemany banks honor them well beyond 180 days but may print a “void after” date or require extra verification. If you’re holding an old check, don’t panichere’s exactly what to do, step by step.

Personal & Business Checks: The 6-Month “Stale Date” Rule

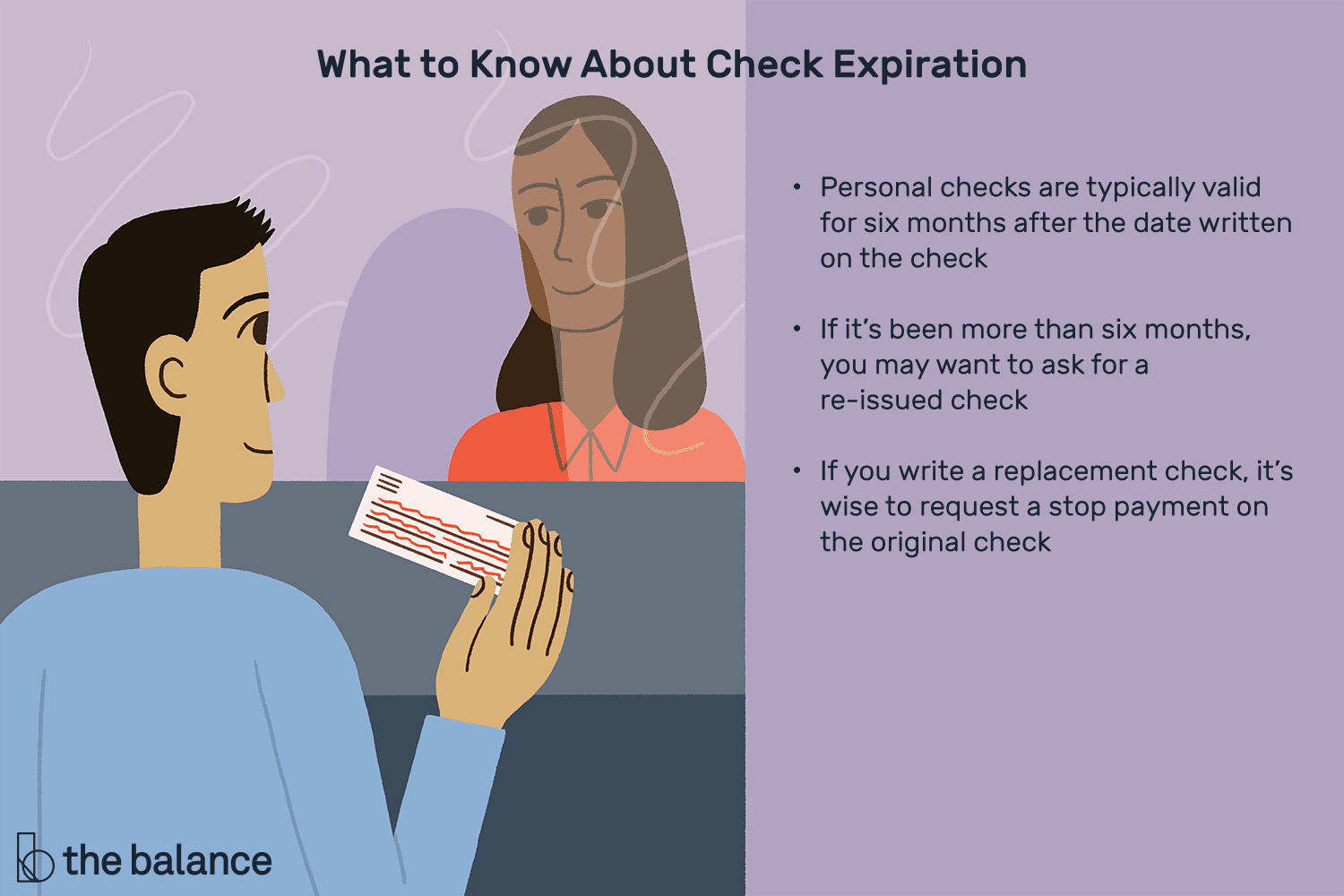

In the U.S., the Uniform Commercial Code (UCC) says a bank is not obligated to pay a check presented more than six months after the date on the checkthough it may pay it in good faith. Translation: after 180 days, it’s the bank’s call. That’s why some old checks clear and others bounce. If you’re the payee, it’s smart to contact the issuer and request a fresh check rather than gambling at the teller window.

Banks often incorporate that rule into their funds-availability policies and can place longer holds or refuse stale-dated deposits. Regulation CC commentary recognizes stale-dated checks as a reason for exception holds, which is why your teller might say, “We need more time.”

Government & Tax Refund Checks: One Year

Checks issued by the U.S. Treasurythink IRS tax refunds, Social Security benefit checks issued as paper, and other federal disbursementsare generally valid for one year from the issue date. If you missed that window, don’t try to cash it; request a reissue from the agency. Treasury specifically labels checks older than one year as “stale-dated.”

Money Orders: It Depends on the Issuer

USPS Money Orders

United States Postal Service money orders do not expire and do not accrue interest or monthly fees. That makes them unusually forgiving if you discover one in a drawer years later.

Western Union & MoneyGram

Western Union and MoneyGram money orders generally don’t expire eitherbut they may assess monthly service charges after a certain period (often after one year), which can reduce the redeemable value. Always check the fine print on the back for the exact fee schedule.

Cashier’s Checks & Certified Checks: Special Creatures

Cashier’s and certified checks are “official checks” drawn on or accepted by a bank. They don’t neatly follow the 6-month rule for ordinary checks. Many banks treat them as valid far longer, yet some print “void after 60/90/180 days” to manage fraud and escheatment risk. Bottom line: policies varylook for any printed expiration and, if it’s old, contact the issuing bank before trying to deposit.

Also note: once a check is certified, the drawer can’t stop payment the same way they could with a regular check; the bank’s obligation is different. That’s one reason payees prefer official checks for large purchases.

Traveler’s Checks: No Expiration

Traveler’s checks have largely faded from everyday use, but if you find an old booklet, good news: American Express states that its Traveler’s Cheques have no expiration date and remain backed by Amex. Redemption logistics have changed, but the underlying value remains.

Unclaimed Property & “Escheatment” for Uncashed Checks

If a check (like a payroll or dividend check) sits uncashed long enough, the issuer may have to turn the funds over to the state as “unclaimed property” after a dormancy periodoften three years, though it varies by state. If that happened to you, search your state’s unclaimed property site to retrieve the funds.

What Happens If You Deposit a Very Old Check?

- Bank may refuse it because it’s stale-dated (common for anything past 180 days).

- Bank may place a long hold under Regulation CC’s exception-hold rules while it verifies the item.

- Bank may accept it if it believes the funds are good and the risk is lowbut this is at the bank’s discretion.

Old Check? Do This First

- Check the date and the type of instrument. Ordinary personal/business check older than 6 months? It’s stale. Official/cashier’s/certified check? Call the issuing bank and ask whether it’s still payable. U.S. Treasury check older than a year? Request reissue.

- Look for printed language. Phrases like “VOID AFTER 90 DAYS” or “NOT VALID AFTER 180 DAYS” matter to many banks, even if the UCC allows payment in good faith.

- Contact the issuer before depositing. It prevents accidental overdrafts for the person who wrote the check and reduces the chance you’ll face a return.

- Ask for a replacement check if needed. For government checks past one year, follow the reissue instructions for the specific agency (e.g., IRS refund checks).

- Mind unclaimed property clocks. If the check was yours but the issuer sent the funds to the state after dormancy, search and claim from the state.

Writers of Checks: Avoid Stale-Date Headaches

If you issued a check that hasn’t been cashed, consider placing a stop-payment and reissuing. Under the UCC, a written stop-payment order is effective for six months (renewable). That helps you prevent surprises if an old check resurfaces. For certified or cashier’s checks, different rules applytalk to your bank about their indemnity process to replace a lost official check.

Frequently Asked “But What About…?”

“Can I cash a 2-year-old personal check?”

Probably not. The bank isn’t required to honor it after six months. Some will consider it with additional verification, but the smoother route is asking the issuer for a new check.

“My cashier’s check says ‘void after 90 days.’ Is it really void?”

It’s complicated. Many banks print a “void after” date to manage risk and escheatment, yet the bank may still examine and decide whether to honor the item. Always call the issuing bank before depositing a long-expired official check.

“Do traveler’s checks from years ago still work?”

Yes, if they’re from American Express, they have no expirationthough you may need to follow Amex’s current redemption process.

Smart Habits: Never Let a Check Go Stale

- Deposit promptly. Don’t give fraudsters or clerical gremlins more time than necessary.

- Switch to electronic payments when possible for government benefits and refundsdirect deposit avoids paper-check timelines altogether.

- Track outstanding checks in your budget app or ledger and follow up with recipients after 30–45 days. (If they lost it, reissue.)

- Know your state’s unclaimed property site in case you need to retrieve funds.

Real-World Scenarios

1) You found a personal check from Februarynow it’s November.

It’s past six months. Call the issuer, explain, and ask for a fresh check. If you try depositing, expect a possible rejection or extended hold.

2) Your IRS refund check from last spring is still unopened.

If it’s under one year old, cash or deposit it now. If it’s older than one year, request a reissue from the IRS/Treasury.

3) You’re holding a MoneyGram money order from two years ago.

It hasn’t expired, but service fees may have reduced the payout. Check the back for fee details and call first.

4) A cashier’s check from a home sale is 10 months old.

Call the issuing bank before depositing. Many will still honor it or provide instructions (sometimes a reissuance process with identification).

Key Takeaways

- Personal/business checks: usually “stale” after 6 months.

- U.S. Treasury checks: valid for 1 year; then request reissue.

- USPS money orders: do not expire.

- Western Union/MoneyGram money orders: no expiration, possible monthly service fees after a year.

- Cashier’s/certified checks: policies vary; verify with the issuing bank.

- Unclaimed property: after dormancy, funds may go to the statesearch and claim.

SEO Recap

Main keyword: how long is a check good for

Related (LSI) keywords: do checks expire, stale-dated check, cashier’s check expiration, government check validity, money order expiration, unclaimed property, stop payment order, Regulation CC holds

Conclusion

Checks aren’t immortal. Regular checks generally lose their shine after 180 days; federal checks fade after a year. Official checks keep their muscle longer but still need a sanity check with the issuer. When in doubt, call first, avoid guesswork, and request a reissue. Your future selfand your bank accountwill thank you.

SEO Meta Bits

sapo: Wondering if an old check still cashes? Here’s the definitive guide: the 6-month UCC stale-date rule for personal checks, the one-year window for U.S. Treasury checks, why USPS money orders never expire, how official checks work, and what to do if funds have been turned over to the state. Use our step-by-step checklist to avoid bounced deposits, long holds, and awkward phone callsand learn exactly who to call for a reissue when you’re past the deadline.

First-Person Lessons: Real-World Experiences With Old Checks

“I once walked a nine-month-old birthday check into my bank thinking, ‘What’s the worst that could happen?’ The teller smiled, tapped a few keys, and said, ‘We’ll need to place an extended holdsince it’s stale-dated, we have to verify the funds with the other bank.’ That single sentence taught me more about Regulation CC than any brochure.” If you’ve ever stood in that line, you know the feeling: the mix of hope, mild embarrassment, and the gnawing suspicion you should’ve deposited sooner. Exception holds are real, and banks can lean on them when a check is over 180 days old. I learned to call first, ask for a supervisor if needed, and bring an alternate plan (mobile deposit with an extended availability estimate, or a request to the issuer for a re-cut check).

On another occasion, a client mailed me a cashier’s check that sat under a pile of paperwork. When I found it months later, the check literally said “VOID AFTER 90 DAYS.” Panic mode. The rescue move was surprisingly simple: I phoned the issuing bank, read them the serial number, and asked whether they would honor it or reissue. They confirmed they could either verify and accept it or reissue after an indemnity process. It took timebut it was fixable. The big lesson: official checks aren’t all the same; always call the bank on the face of the check.

Friends have similar stories with money orders. A cousin discovered a dusty MoneyGram money order in a moving box. Good news: no expiration. Bad news: monthly service charges had nibbled away at the value after the first year. She still got most of it back, but not all. Now, whenever someone insists on paying me with a money order, I cash or deposit it quicklyand I always read the fee language printed on the back.

One of the more nerve-wracking moments was an IRS refund check that went missing in the mail. When it finally arrivedmore than a year late due to the address snafuit was already past the Treasury’s one-year window. The fix involved requesting a reissue via the agency’s prescribed process. It wasn’t fun, but it was straightforward once I knew the one-year rule exists for federal checks. Now I opt into direct deposit for any government payments to eliminate paper delays entirely.

I’ve also been on the other sideas the person who wrote a check that wasn’t cashed for months. The anxiety kicks in around day 45: “Do I keep those funds parked forever?” My solution: set a reminder at day 60 to follow up with the payee. If they can’t find the check, I issue a replacement and, for safety, place a stop-payment on the original (and renew it if needed). That way, if the old one pops up later, it won’t surprise my balance. The UCC’s six-month stop-payment window is a helpful guardrail.

Finally, unclaimed property is a twist many people don’t expect. A company-issued check you never cashed can get reported to the state after dormancy (often around three years). I’ve helped friends recover money by searching their state’s unclaimed property portal. It’s oddly satisfyinglike a digital scavenger hunt where the prize is cash you forgot you had. The moral: if you’ve moved, update your address with employers and financial institutions, and make an annual habit of checking your state’s site.

The overarching theme from all these episodes is simple: speed and communication win. Deposit checks quickly, switch to electronic payments where possible, and when something’s old, pick up the phone. Policies vary, but friendly verification calls and clear requests (“Can you reissue?”) save time, fees, and awkwardness. And if you’re staring at a paper relic from the last decadesay, a traveler’s checkdon’t assume it’s worthless. Some instruments truly never expire; they just require a modern path to redemption.