Real estate commissions can feel like the mysterious line item that sneaks into a closing statement wearing sunglasses and a fake mustache. You know it matters. You know it can be thousandsor tens of thousandsof dollars. But unless you work with home sales every day, the math may look more complicated than it really is.

Good news: calculating real estate commissions is mostly simple multiplication, plus a little contract-reading, a little market awareness, and a healthy respect for the phrase “negotiable.” In the United States, real estate commission rates are not fixed by law. They vary by location, brokerage, property type, agent agreement, and whether the seller, buyer, or both sides agree to pay certain fees.

This guide explains how to calculate real estate commissions in 10 practical steps, using plain English, real examples, and enough math to be useful without making your calculator file a complaint.

What Is a Real Estate Commission?

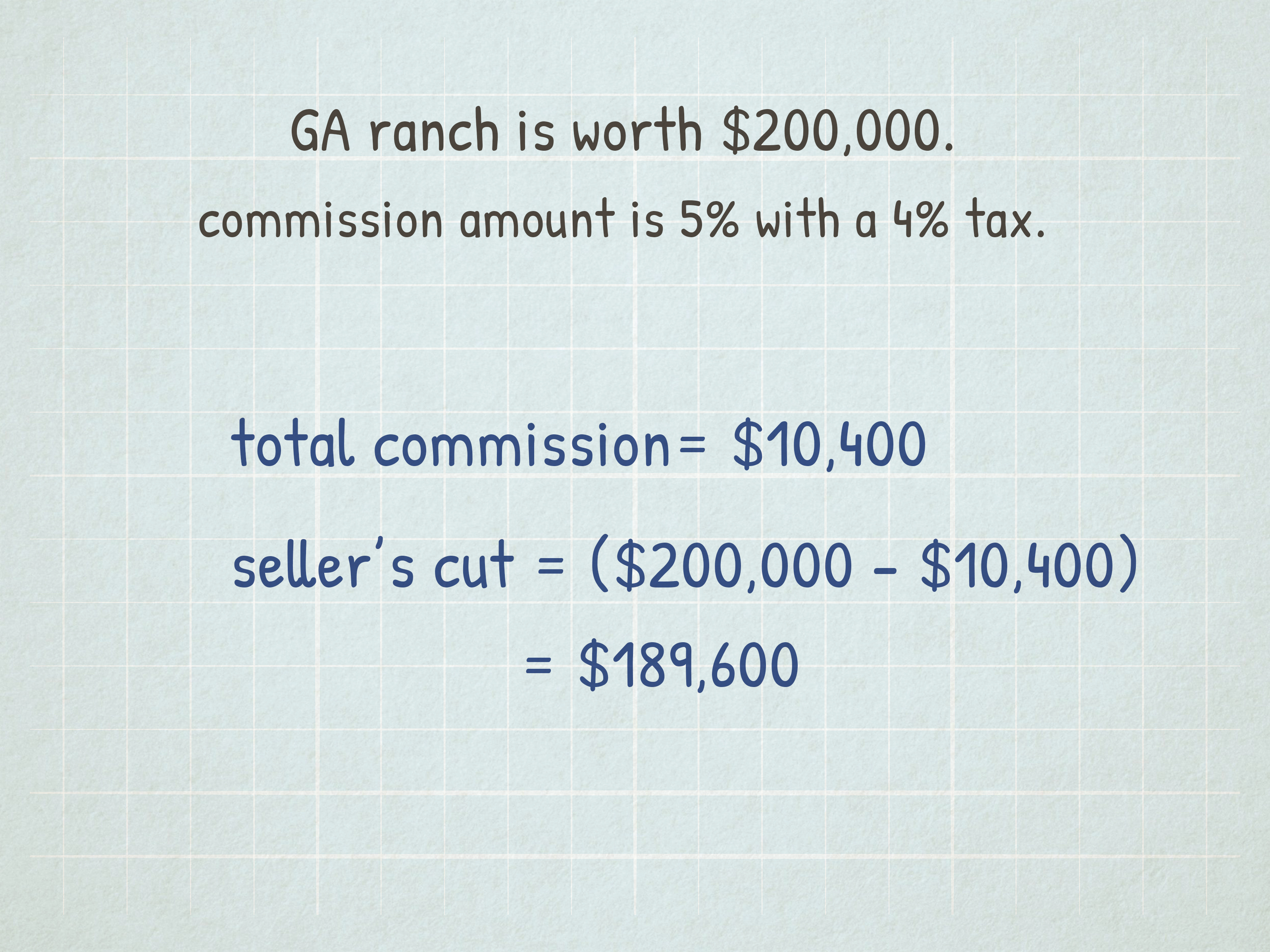

A real estate commission is a fee paid to real estate professionals for helping complete a property transaction. Traditionally, the fee has often been calculated as a percentage of the home’s final sale price. For example, if a home sells for $500,000 and the total commission is 5%, the total commission equals $25,000.

That amount may be split between the listing agent’s brokerage and the buyer’s agent’s brokerage, and then each agent may split their side with their broker according to their own brokerage agreement. In other words, the commission shown on the closing statement is not always the amount an individual agent personally takes home.

Since the 2024 real estate commission rule changes connected to the National Association of Realtors settlement, buyers and sellers have been paying closer attention to exactly who pays what. Sellers may still choose to offer compensation to a buyer’s agent, but buyer-agent compensation is no longer supposed to be advertised through many MLS systems in the same old way. Buyers working with an agent generally need a written agreement explaining services and compensation before touring homes.

How to Calculate Real Estate Commissions: 10 Steps

Step 1: Start With the Final Sale Price

The most important number in the commission calculation is the final sale price, not the original listing price, the Zestimate your cousin quoted at Thanksgiving, or the “I know what I’ve got” price from the seller’s group chat.

Use the actual contract price or expected sale price. If you are estimating before an offer is accepted, use a realistic projected sale price based on recent comparable sales.

Example: A home is listed for $525,000 but sells after negotiation for $510,000. Commission is calculated using $510,000 unless the listing agreement states otherwise.

Step 2: Identify the Total Commission Rate

Next, identify the total commission rate. In many traditional transactions, total real estate commissions have often landed around 5% to 6% of the sale price, but that is only a common rangenot a rule. Some sellers negotiate a lower listing fee. Some brokerages offer flat-fee or reduced-fee models. Some luxury or high-price transactions may have different structures. Some buyer agreements may use a percentage, flat fee, hourly fee, or minimum compensation amount.

The key is simple: do not assume. Read the listing agreement, buyer representation agreement, purchase contract, and closing disclosure.

Formula:

Total Commission = Sale Price × Total Commission Rate

Example: $510,000 × 5.5% = $28,050 total commission.

Step 3: Convert the Percentage Into a Decimal

Before multiplying, convert the commission percentage into a decimal. This is where many mistakes happen, usually because percentages like to pretend they are friendlier than they are.

To convert a percentage to a decimal, divide by 100:

- 6% becomes 0.06

- 5.5% becomes 0.055

- 3% becomes 0.03

- 2.5% becomes 0.025

Example: If the agreed listing-side commission is 2.75%, multiply the sale price by 0.0275.

$510,000 × 0.0275 = $14,025

Step 4: Separate the Listing-Agent Side and Buyer-Agent Side

In many transactions, the total commission is divided between two sides: the listing side and the buyer side. These sides may be equal, but they do not have to be.

For example, a transaction may include:

- 2.75% to the listing broker

- 2.5% to the buyer broker

- 5.25% total commission

Using a $510,000 sale price:

$510,000 × 0.0275 = $14,025 listing-side commission

$510,000 × 0.025 = $12,750 buyer-side commission

$14,025 + $12,750 = $26,775 total commission

This split matters because current rules and contracts may place more responsibility on buyers to understand their agent’s compensation. A buyer may negotiate for the seller to pay the buyer-agent fee as part of the offer, but it should be clearly written into the agreement.

Step 5: Check Who Is Actually Paying the Commission

Historically, sellers often paid the total commission from sale proceeds. Economically, buyers still contributed indirectly because the sale price funds the transaction. Today, the practical payment arrangement can vary more visibly.

Common scenarios include:

- The seller pays the listing agent and agrees to pay some or all of the buyer-agent compensation.

- The seller pays only the listing agent, while the buyer pays their own agent directly.

- The buyer requests seller concessions or a price adjustment to help cover representation costs.

- The buyer-agent fee is handled through a separate written buyer agreement.

Always confirm the payment source in writing. A verbal “don’t worry about it” is not a financial plan. It is a future argument wearing comfortable shoes.

Step 6: Calculate Seller Net Proceeds

For sellers, commission is only one part of the net proceeds calculation. Net proceeds are the amount the seller expects to receive after paying commissions, mortgage payoff, closing costs, taxes, transfer fees, repairs, concessions, and other obligations.

Basic seller net formula:

Seller Net Proceeds = Sale Price − Commission − Mortgage Payoff − Seller Closing Costs − Credits/Concessions

Example:

- Sale price: $510,000

- Total commission: $26,775

- Mortgage payoff: $310,000

- Seller closing costs and transfer taxes: $6,500

- Seller credit to buyer: $5,000

$510,000 − $26,775 − $310,000 − $6,500 − $5,000 = $161,725

In this example, the seller’s estimated net proceeds are $161,725. That number is far more useful than simply knowing the home sold for $510,000.

Step 7: Calculate Buyer Out-of-Pocket Costs

Buyers should also calculate commission exposure, especially if their agreement says they owe their agent a fee that is not fully covered by the seller.

Example: A buyer signs an agreement to pay their agent 2.5% of the purchase price. The home sells for $510,000. The seller agrees to pay 2% toward buyer-agent compensation.

Buyer-agent fee owed:

$510,000 × 0.025 = $12,750

Seller-paid amount:

$510,000 × 0.02 = $10,200

Buyer remaining responsibility:

$12,750 − $10,200 = $2,550

That $2,550 may need to be paid at closing unless the contract, lender rules, or negotiated terms allow another arrangement. Buyers should ask their lender early whether a commission-related cost can be financed, credited, or must be paid separately. Loan-program rules matter.

Step 8: Consider Flat Fees, Minimum Fees, and Tiered Rates

Not all commission agreements are a clean percentage. Some agents and brokerages use alternative compensation models, including flat fees, limited-service packages, hourly consulting, rebates where legal, or tiered commission structures.

Flat-fee example: A seller pays a $5,000 listing fee instead of a percentage. If the home sells for $400,000, the listing fee equals 1.25% of the sale price.

$5,000 ÷ $400,000 = 0.0125, or 1.25%

Minimum-fee example: A buyer agreement says the buyer’s agent earns 2.5% or $8,000, whichever is greater. If the buyer purchases a $250,000 condo:

$250,000 × 0.025 = $6,250

Because the minimum is $8,000, the commission owed would be $8,000, not $6,250.

Tiered-rate example: A listing agreement may say 3% on the first $500,000 and 2% on any amount above $500,000. If a home sells for $650,000:

$500,000 × 0.03 = $15,000

$150,000 × 0.02 = $3,000

$15,000 + $3,000 = $18,000

This is why reading the agreement matters. The math is easy; discovering the correct math is the real sport.

Step 9: Factor in Concessions, Credits, and Loan Limits

Seller concessions can affect the overall deal. A seller might agree to pay closing costs, offer a repair credit, contribute to a rate buydown, or help cover buyer-agent compensation. However, mortgage programs often limit how much sellers and other interested parties can contribute toward a buyer’s costs.

For example, conventional loan guidelines may limit interested-party contributions based on the buyer’s down payment, occupancy type, and loan-to-value ratio. The important takeaway is this: a concession that sounds simple in negotiation may require lender approval before closing.

Buyers and sellers should ask the lender, title company, and real estate professionals how each credit will appear on the closing disclosure. A commission agreement that works on paper still needs to survive the underwriting and closing process.

Step 10: Review the Closing Disclosure Before Closing

The final step is to verify the numbers on the closing disclosure or settlement statement. This document shows the actual charges, credits, and cash due at closing. For sellers, it helps confirm how much will be deducted from sale proceeds. For buyers, it shows the final cash-to-close figure.

Check these items carefully:

- Sale price

- Listing broker commission

- Buyer broker commission, if applicable

- Seller credits or concessions

- Loan costs

- Title and escrow fees

- Transfer taxes and recording fees

- Prorated taxes, HOA dues, or assessments

- Final cash to close or seller proceeds

If something looks wrong, ask before signing. Closing day is not the best time to practice silent suffering. A simple question can prevent an expensive misunderstanding.

Real Estate Commission Calculation Examples

Example 1: Traditional Percentage Commission

A seller sells a home for $600,000. The agreed total commission is 5.5%.

$600,000 × 0.055 = $33,000

If the commission is split as 2.75% to each side:

$600,000 × 0.0275 = $16,500

Each side receives $16,500 before any brokerage splits or additional internal fees.

Example 2: Uneven Commission Split

A home sells for $450,000. The listing side earns 3%, and the buyer side receives 2% paid by the seller.

$450,000 × 0.03 = $13,500

$450,000 × 0.02 = $9,000

$13,500 + $9,000 = $22,500 total seller-paid commission

Example 3: Buyer Pays the Difference

A buyer agreement requires 2.5% compensation. The seller offers 1.5%. The purchase price is $380,000.

Total buyer-agent compensation:

$380,000 × 0.025 = $9,500

Seller contribution:

$380,000 × 0.015 = $5,700

Buyer responsibility:

$9,500 − $5,700 = $3,800

This is exactly the kind of calculation buyers should do before making an offer, not after they have already emotionally moved their imaginary couch into the living room.

Common Mistakes When Calculating Real Estate Commissions

Mistake 1: Using the Listing Price Instead of the Sale Price

Commission is usually based on the final sale price. If the property sells below or above the list price, the commission changes accordingly.

Mistake 2: Assuming Every Commission Is 6%

Many people still say “the commission is always 6%,” but that is not accurate. Commission rates are negotiable and vary by market, property type, agent, and service level.

Mistake 3: Forgetting Buyer Agreements

Buyers now need to pay close attention to written buyer agreements. The agreement may say how the buyer’s agent is paid, what happens if the seller pays less than expected, and whether the buyer owes the difference.

Mistake 4: Ignoring Broker Splits

If you are an agent calculating your personal income, do not confuse gross commission with take-home commission. Your brokerage split, transaction fees, referral fees, taxes, marketing costs, and team split can all reduce your final amount.

Mistake 5: Not Checking the Closing Disclosure

Even if the agreement was correct, numbers can be entered incorrectly. Always compare the closing disclosure with the contract and commission agreement.

How Agents Calculate Their Own Commission Income

From an agent’s perspective, gross commission income is only the first step. Suppose an agent’s side of the commission is $15,000. If the agent has a 70/30 split with their brokerage, the agent receives 70% before taxes and expenses.

$15,000 × 0.70 = $10,500

If the agent also pays a $500 transaction fee and a 25% referral fee, the math changes quickly.

Referral fee:

$15,000 × 0.25 = $3,750

Remaining after referral:

$15,000 − $3,750 = $11,250

Agent share after 70/30 split:

$11,250 × 0.70 = $7,875

After transaction fee:

$7,875 − $500 = $7,375

That is before income taxes, self-employment taxes, insurance, gas, signs, photography contributions, software, lead costs, and the emotional cost of answering “Is this still available?” at 11:47 p.m.

Can You Negotiate Real Estate Commissions?

Yes. Real estate commissions are negotiable. That does not mean every agent will accept every offer, but buyers and sellers can ask questions, compare services, and request different fee structures.

Smart questions include:

- What services are included in your fee?

- Is your commission a percentage, flat fee, minimum fee, or tiered structure?

- Who pays the buyer-agent compensation?

- What happens if the seller offers less than the buyer-agent agreement requires?

- Are there administrative, transaction, marketing, or cancellation fees?

- Will the commission change if you represent both sides, where legally allowed?

- Can I review a net sheet before signing?

The goal is not to pick the cheapest agent automatically. The goal is to understand the value, services, strategy, and cost before making a decision.

of Practical Experience: What Real Commission Math Looks Like in the Real World

In real life, calculating real estate commissions is rarely just about multiplying one number by another. The math is simple, but the context is where people get surprised. One of the most common experiences for sellers is realizing that a “small” percentage difference can become a big dollar difference at modern home prices. A half-percent difference on a $700,000 home equals $3,500. That is not pocket change. That is a refrigerator, several mortgage payments, or enough moving boxes to make your garage look like a cardboard city.

Sellers often benefit from asking for a seller net sheet before listing the home. A net sheet estimates sale price, commission, mortgage payoff, title costs, transfer taxes, escrow fees, prorations, repairs, and seller credits. The first version will not be perfect, but it gives the seller a financial map. Without that map, it is easy to celebrate a high offer and later discover that concessions, repairs, and commissions reduced the final proceeds more than expected.

Buyers, meanwhile, should treat the written buyer agreement like a budget document, not just a formality. If the agreement says the buyer’s agent earns 2.5%, the buyer should ask what happens if the seller offers 0%, 1%, or a flat amount. A buyer who skips this question may be surprised by a cash-to-close increase. In competitive markets, this can affect affordability just as much as inspection repairs or appraisal gaps.

Another real-world lesson: the highest offer is not always the best offer. Imagine two buyers. Buyer A offers $505,000 but asks the seller to pay $15,000 in credits and buyer-agent compensation. Buyer B offers $495,000 but asks for only $3,000 in seller-paid costs. Depending on the commission structure, repairs, financing strength, and appraisal risk, Buyer B may produce a better net result for the seller. This is why experienced listing agents prepare offer comparison sheets instead of simply pointing at the biggest number and shouting, “Winner!”

For agents, commission calculations are also a reminder that gross income is not net income. A $20,000 commission can shrink after brokerage splits, referral fees, marketing costs, transaction fees, taxes, licensing expenses, association dues, lockbox fees, software, photography, mileage, and unpaid time spent with clients who never buy or sell. Consumers do not need to memorize an agent’s business expenses, but understanding the difference between gross commission and take-home pay helps explain why service levels vary.

Finally, the best commission conversations happen early. Sellers should discuss fees before signing the listing agreement. Buyers should discuss compensation before touring homes. Both sides should revisit the numbers before submitting or accepting an offer. The people who get into trouble are usually not bad at math; they are late to the math. Real estate rewards people who ask clear questions before the closing table, because by then the pens are out, the moving truck is booked, and nobody wants a surprise invoice doing jazz hands in the corner.

Conclusion

Learning how to calculate real estate commissions gives buyers and sellers more control over one of the largest costs in a home sale. The basic formula is simple: multiply the sale price by the agreed commission rate. The smarter move is to go furtherseparate each side of the commission, confirm who pays, review buyer agreements, calculate net proceeds, check seller concessions, and verify everything on the closing disclosure.

Real estate commissions are negotiable, but negotiable does not mean random. The right commission depends on market conditions, property value, service level, agent experience, and the written agreements between the parties. Whether you are selling a starter home, buying your first condo, or calculating an agent’s gross commission income, the best tool is not just a calculator. It is a calculator plus a contract, a clear conversation, and maybe one strong cup of coffee.

Note: This article is for educational publishing purposes only. Real estate commission practices, contract forms, lending rules, and closing customs vary by state, brokerage, transaction type, and local market. Buyers and sellers should confirm details with their real estate professional, lender, title company, or qualified legal adviser before making financial decisions.